Crop Insurance Continues to Earn the Trust of America’s Farmers and Ranchers

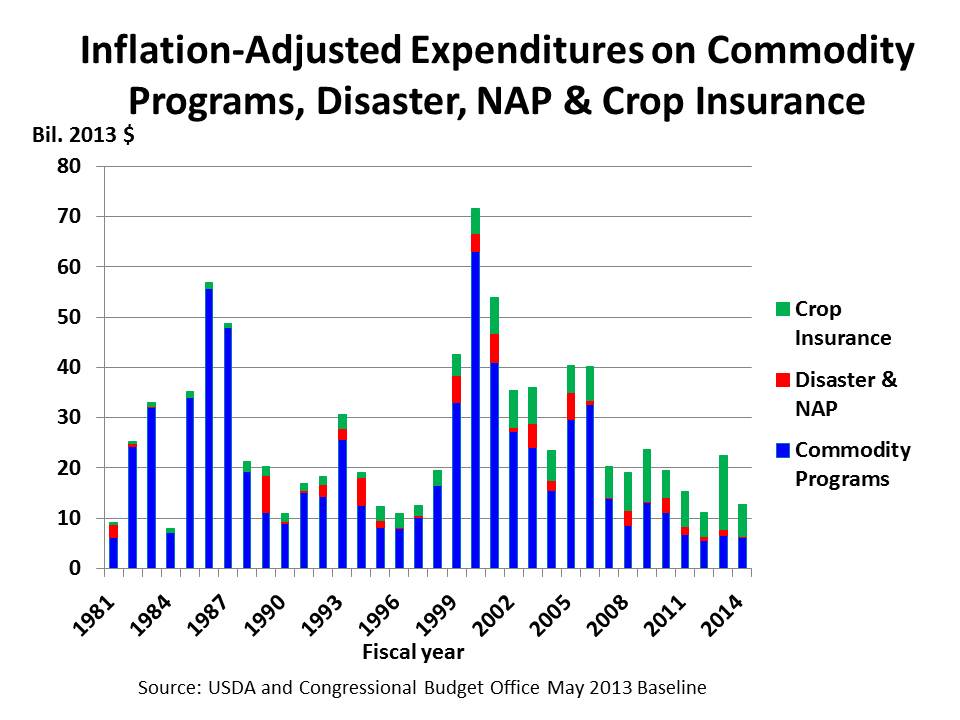

As agriculture faces new challenges and a changing climate, crop insurance remains the number one risk management tool for America’s farmers and ranchers, according to the chair of National Crop Insurance Services (NCIS). Last year, crop insurance protected a record 460 million acres of farmland and more than $137 billion in food, fiber, and fuel.

Kendall Jones, chair of NCIS and president and CEO of ProAg, made her remarks at the start of the industry’s annual meeting in California.

“The scale and size of crop insurance further demonstrate that farmers have come to rely upon our industry when the going gets tough,” she said. “We need to build on that credibility as the environment farmers operate in continues to evolve. We are in position to continue to modernize and improve – adapting risk management tools to the risk.”

Farmers invested $5 billion dollars of their own money through premiums in 2021 to protect their crops. Jones said the increasing popularity of crop insurance should come as no surprise.

“The crop insurance industry has established credibility with farmers and policymakers. It all starts with trust,” she said. “The American farmers and ranchers rely on the crop insurance industry to be there when they need us as they set up their operating loans, in times of natural weather disasters or during financial distress from market pressure.”

Among the most highly discussed topics of the conference was how the industry is improving to meet the changing needs of agriculture. Jones praised the data-driven nature of crop insurance, explaining that it has made crop insurance uniquely adept at helping America’s farmers respond to climate change.

“As farmers deal with new challenges, it is important to maintain the integrity and credibility of the Federal crop insurance program, but we need to acknowledge it will not stay the same,” she said.

Jones pointed to the work that the crop insurance industry has done alongside the U.S. Department of Agriculture to facilitate the voluntary adoption of climate-smart agriculture and champion more diversity and equity within agriculture.

She set the stage for the upcoming Farm Bill debate by noting the large percentages of new members in both the Senate and House agriculture committees along with changes in leadership in both committees.

Recently, a diverse coalition representing 55 farming, banking, and conservation organizations called on government officials to oppose cuts to crop insurance in the Farm Bill. The coalition delivered letters to the House and Senate budget and appropriations committees, as well as to the Secretary of Agriculture and Acting Director of the Office of Management and Budget, emphasizing the importance of crop insurance as a risk management tool.

“There are always new ideas from new voices to be heard in the Farm Bill discussion,” she said. “How we share our collective story and listen to their perspectives will help influence the process.”